In 2007, Warren Buffett – the person may consider being the most successful stock picker of all time – made a $1 million bet with Ted Seides, a founder of Protégé Partners.((Longbets.org: Over a ten-year period commencing on January 1, 2008, and ending on December 31, 2017, the S&P 500 will outperform a portfolio of funds of hedge funds, when performance is measured on a basis net of fees, costs and expenses.))

Buffett wagered that a passively managed index fund would perform better than a collection of hedge funds over the subsequent ten years (January 1, 2008 to December 31, 2017).

It was a surprising wager since Buffett is also known for his position that “Diversification (a popular investment technique of reducing risk in the stock market) is protection against ignorance.”((Warren Buffett on the Folly of Diversification))

Since making the bet, Buffett has consistently recommended that the average investor forego individual stocks and dismiss their belief that they can beat the market.

When asked at the 2008 Berkshire-Hathaway shareholder meeting where to invest “your first million dollars,” he replied, “I’d put it all in a low-cost index fund that tracks the S&P 500 and get back to work [at my regular job].”

No hypocrite, Buffett puts his money where his mouth is.

He shows by his actions that he believes what he says.

Buffett revealed during a CNBC interview that he had instructed the executor of his estate to invest 90 percent of his money into the S&P 500 index fund for his wife after he dies.

Table of Contents

What is an Index Fund?

An index fund is a fund with a portfolio designed to match or track a financial market index such as the Standard & Poor’s 500 Index((Standard & Poor’s 500 Index)), Dow Jones Industrial Average (DJIA)((Dow Jones Industrial Average (DJIA))), or the Nasdaq Composite((Nasdaq Composite)).

Unlike managed portfolios whose holdings are selected and managed by professional analysts and managers, an index fund invests in the stocks included in the designated index.

For example, an S&P 500 index fund would own the 500 stocks of the companies making up the index while a DJIA index fund would have the thirty stocks composing the Dow Jones Industrial Average.

Why Invest in Index Funds?

An investor today is faced with a bewildering menu of potential investments.

One expert recommends buying gold and precious metals. Another guru claims that real estate – residential and commercial – is the best choice, while a third suggests that AAA-rated corporate bonds are the path to long-term wealth. A few suggest that an apocalypse is coming, so saving or investment for the future is futile, regardless of the investment type.

Most predictions rely on a little bit of truth and a great deal of conjecture.

Forecasting how any investment will fare in the future is akin to finding a black cat in a dark room while blindfolded and not sure the cat is in the space. For that reason, Winston Churchill noted that prophecies are best done after an event has occurred.

Most investments have had their place in the sun at one time or another. The ideal investment depends on the investor’s goals, amount and pattern of financing, and risk profile (the willingness to accept a loss). Even so, the best investment choice for most long-term investors is an index fund.

Reasons to Save

Life requires accepting the risk of the unknown future, the only certainty being eventual death.

In a lifetime, everyone experiences triumphs and failures, cycles of plenty and distress.

Experience has taught us that we need to save a portion of our income during the good times to build the necessary resources for the bad times.

Some adversities, such as the Covid-19 pandemic, are unexpected. Unemployment soared around the world, forcing people to adjust to new lifestyles unless they had set aside sufficient capital to replace their lost income.

On the other hand, aging affects everyone, usually leading to retirement and lower-income.

Despite the inevitability of reduced income, most people fail to prepare for the event.

The United States has the most robust economy and the highest per capita income of industrialized countries. Yet, one-quarter of retired Americans, according to the American Association of Retired Persons (AARP), depend on Social Security payments for their income while the payments represent more than half of the retirement income for another fifty percent.((GDP per capita (current US$) – United States)),((12 Top Things to Know About Social Security))

People should save and invest a portion of their income during their earning years to have the life they want when they quit working.

The Value of Consistent Investment

Establishing the habit of saving and investing early in life is essential. A person who begins investing at age 25 for retirement has substantially more capital at age 65 than the one who starts at age 45.

The following Table 3.1 illustrates the difference, even though both invest $100 monthly and earn the same rate of return (3%) on their investment:

Table 3.1 Invest Early to Build a Fortune

In each case, the contributed capital earns a return added to the amounts provided by the investor. Due to the longer investment and compounding period of Investor A, Investor B would need to invest $380 – an extra $280 – per month for the twenty years to equal the total investment value ($92,937) owned by Investor A. With no additional investment, his monthly payment for the same fifteen-year period of Investor A will be $227.

Investment Return Makes a BIG Difference

Investment return is a function of risk in most cases: the more risk the investor is willing to assume, the higher his potential return.

- Saving accounts. A U.S. savings account is considered one of the safer possible investments, due to the U.S. Government’s guarantee of principal protection up to $250,000 per depositor.((Understanding Deposit Insurance))

- Bonds. Debt instruments are considered safer than an investment in common stock since bondholders have a priority on corporate assets in the event of dissolution or failure. (Potential bond purchasers need to recognize that the principal is not repaid until maturity and the market price of a bond will vary with market interest rates and the coupon on the bond.

- Common stocks. Equities are considered higher risk since their return is tied solely to the profitability of the issuing corporation. Common stocks generally provide a higher return for assuming a higher risk.

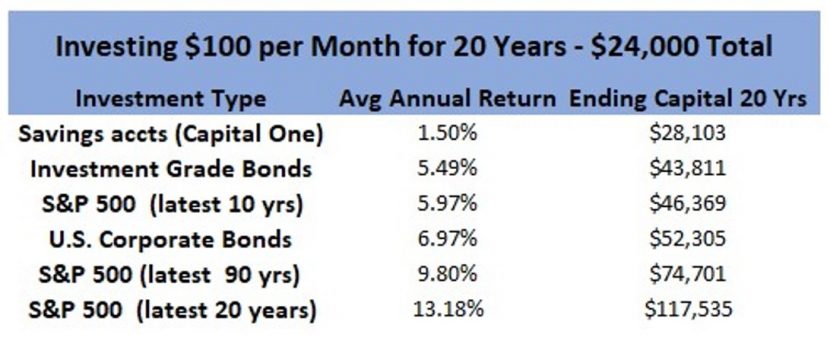

Table 3.2 illustrates the difference in actual historical returns for a variety of investment options. The column titled “Ending Capital 20 Yrs” illustrates the difference between the various investment options.

Table 3.2 Investment Types and Returns

Advantages of Index Fund Investment

There are an estimated 630,000 publicly traded companies and sixty major stock exchanges in the world today, including about 4,000 listed on stock exchanges in the United States and an additional 3,300 whose securities trade on NASDAQ. (A few companies are present in both markets.)

During a typical calendar year, some companies’ stocks will increase while others decrease by varying degrees. Some companies go out of business while others offer their shares to the public for the first time.

The combination of technological advances, changing trade conditions, international politics, and erratic consumer preferences continuously affect the profitability, even the existence, of market leaders from one decade to the next.

Major brick-and-mortar retailers like Sears and J.C. Penny Company struggle to survive in the growth of online retailers like Amazon.

Major airlines have sought government financing to stay alive, and once-dominant American automakers have lost large chunks of market share to foreign manufacturers.

An investor trying to select a single or a few individual companies for long-term investment faces enormous obstacles in collecting and analyzing reams of financial information and projections on different companies, their competitors, and the industry in which they participate in addition to remaining current on political, economic, and natural events that affect their future.

Professional analysts and investment advisers often take contrary positions on whether to buy, hold, or sell the same company’s securities.

Christopher Browne, a partner in the New York brokerage firm Tweedy, Browne Company LLC, and author of “The Little Book of Value Investing,” claims, “Value investing requires more effort than brains and a lot of patience. It is more grunt work than rocket science.” Investing in individual stocks of companies requires hours of research and learning the skills to be successful.((Secrets Of Success: Effort, not brains, key to value investing)),((10 things I learned from The Little Book of Value Investing by Christopher H. Browne))

A wrong choice – an error in judgment – can be disastrous for beginning investors trying to build a retirement portfolio or save for future college expenses. A better solution is investing in an index fund with less risk and more certainty of a positive return.

The main advantages of the index fund versus individual stocks or actively managed portfolios are:

Diversification

Spreading the risk is the primary tool of insurance companies and professional fund managers alike. Index funds, by definition, spread the risk of owning a single security over the universe of securities included in the index.

The number of different companies in an index varies according to the purpose of the index.

An S&P 500 index fund consists of 500 stocks that make up the S&P 500 Index. A DJIA index fund is made up of the thirty stocks contained in the index.

An investor’s return in a single corporation is wholly on the result of price movement of that business’s common stock influenced by actual financial results and other investors’ opinions of those results.

The composition of each index, i.e., the individual stocks included in the calculation of value, is publicly reported. An investor in an index fund benefits from the aggregate price movements of the different company shares in the index.

The return is always the average, never as good as the best performer, but never as bad as the worst.

Low Expenses

Unlike public managed funds with fees between 1.0% and 2.5% of the portfolio value or a hedge fund with the same level of management fees plus a percentage of profits, index fund fees are typically below 0.2%.

The difference in costs is a big reason that managed funds have difficult times matching the long-term return of the passively managed index funds.

Long-term Returns

The average annual return of the S&P 500 has 9.8% for ninety years, considerably better than savings accounts or corporate bonds.

Investopedia, a popular financial education site, notes that the stock market measured by the S&P 500 has outperformed all other types of financial securities and the housing market over the past century when investing for five or more years.

Between 1945 and 1995, only a few five-year periods would have resulted in a loss in the S&P 500. A 10-year holding period performed even better, with returns averaging about 13%—with zero negative returns. So the longer the holding period, the more likely you are to make money.((Which Investments Have the Highest Historical Returns?))

Investors who choose to invest short-term or in index funds with a narrow focus – a specific industry, market size, etc. – will experience more variability in return than a broad market index funds.

History of Index Funds

In the past, when clients questioned the poor performance of their investment when the stock market as a whole is in a trend of rising prices, brokers and investment advisers replied, “It is not a ‘stock market,’ but a market of individual stocks.”

They explained that the stock market was just an average calculated from the price movements of the individual stocks making up a specific index. No one owns the “stock market” and trying to maintain a portfolio of stocks that would accurately reflect any index’s price changes in real-time would be almost impossible.

For years, the advisers were right.

The information and technology did not exist to track broad portfolios in real-time and take appropriate action to quickly eliminate variances between a stock portfolio and the index it represented.

Stock investors either relied on rumors, brokerage firms’ analyses, and skill to invest in individual companies or hired a professional investment adviser who would manage their funds for a fee.

Some questioned the appeal of an index fund, wondering, “Why anyone would be satisfied with an average return?“

One of the key claims of the professionals was those who followed their advice could outperform the averages.

Investment advisers and stockbrokers publicized their research and investment results with slick brochures, brightly colored graphs, and emotional television commercials.((Dean Witter | Television Commercial | 1997))

Edward Johnson, then chairman of Fidelity Investments (the largest mutual fund company in the world), publicly stated that he could not “believe that the great mass of investors are [sic] going to be satisfied with receiving just average returns.”((Ferri, R. All About Index Funds: The Easy Way to Get Started. McGraw-Hill Education; 2nd edition. January 12, 2007.))

In 1973, several academic studies appeared that challenged the claim that professional managers could beat the market, setting off a revolution in fund management that continues to this day.((A Random Walk Down Wall Street: The Time-Tested Strategy for Successful Investing (Ninth Edition) Paperback – December 17, 2007))

Jack Bogle – Father of Index Funds

An economics major from Princeton University cum laude, Bogle is best known as the father of the index fund.

In 1976, He created the Vanguard 500 Index Fund.((Vanguard 500 Index Fund Investor Shares (VFINX)))

Bogle questioned the investment strategy of selecting individual stocks or attempting to buy when prices were low and sell when prices were high, recognizing that any managed portfolio’s logical futility of beating an index fund long-term is virtually impossible.

Most actively managed funds underperform the market.((Liu, B. SPIVA U.S. year-end 2019 scorecard: active funds continue to lag. S&P Global website. April 8, 2020 (Accessed June 15, 2020). https://www.spglobal.com/en/research-insights/articles/spiva-u-s-year-end-2019-scorecard-active-funds-continued-to-lag)) No one has demonstrated a consistent ability to call price trends or reversal of trends on any long-term basis.

As Dr. Philip Lawton, CFA, observed in his article Calling the Turns: Why Market Timing is Do Hard:

The stock market’s turning points, as well as the valuation peaks and troughs of individual stocks, increasingly appear to be driven more by mass psychology than by sober professional judgment based on disciplined valuation techniques.((Calling the Turns: Why Market Timing Is So Hard by Philip Lawton, Ph.D., CFA))

Even professional investors are affected by their emotions and behavioral and cognitive biases.

Rumors, false or missing information, economic, and natural events affect investor psychology in the short-term. For example, few investors have no regretted selling a stock too soon or, conversely, too late.

Bogle believed that stock prices in the long-term reflect the company’s intrinsic value.

Bogle and Buffet agreed that an investment in an index fund of the biggest and best U.S. companies reflects confidence in the American spirit and economy.

Even though issues appear from time to time, the country and its leaders have the vitality, persistence, and knowledge to prevail.

While likening investing in the stock market to wagering is always a misnomer, a comparison to horse racing might help to understand the difference between buying a single stock and an index fund.

An investor in a single stock is like making a bet on the winner of the race while a purchaser of an index fund bets that every horse in the field will finish the race.

Picking the winner may offer the highest pay-off but with a higher likelihood of a total loss. Selecting the field has less reward, but virtually no chance of loss.

Vanguard 500 Index Fund

Bogle’s strategy was to create a portfolio of stocks of companies in the First Index Investment Trust, now the Standard & Poor’s 500 Index.

The investment in each company is in the same proportion as its weighting in the index. Limiting the portfolio’s active management allowed him to charge fees 50%-60% below his competitors’ managed fund fees.

He implemented a no-load distribution structure for an additional cost advantage (no commission costs on purchase).

The fund began with just $11 million in assets but grew to more than $100 billion by November 1999. The fund continued to grow, reach almost $500 billion in May 2020.

While competitors subsequently developed index funds as a competitive necessity (including the Fidelity Group), Bogle’s original fund continues to be popular with investors delivering an average annual return of 12.81% for the ten-year ending June 15, 2020.((Vanguard 500 Index Investor (VFINX). YCharts website. (Accessed June 16, 2020) https://ycharts.com/mutual_funds/M:VFINX)),((Fidelity® 500 Index Fund))

The Evolution of Index Funds

Since the first index fund appeared in 1976, index funds of multiple types have exploded in number. All retain their passive management strategy and low management fees but track different security indexes.

Types include:

- Broad market. These funds give investors the broadest possible market exposure and diversification in U.S. companies and track the CRSP U.S. Total Market Index or the Dow Jones U.S. Total Market Index.((CRSP U.S. Total Market Index)),((Dow Jones U.S. Total Stock Market Index))

- International. The choices range from funds that track the world equity markets (FTSE All-World ex U.S. Index), emerging or frontier markets (FTSE Emerging Index), or a specific geographic region such as the Pacific (MCSI Pacific Investible Market Index).((FTSE All World ex US Index)),((FTSE Emerging Index)),((MSCI Pacific IMI (USD)))

- Market Cap. There are index funds composed of large companies that track the S&P 500, medium-sized companies that follow the Russell Midcap Index, and small-sized public companies (Morningstar Small Core Index).((Russell Mid Cap Index))

- Growth. These funds hold securities of companies with expected earnings growth above the market average. They track the CRSP U.S. Large-Cap Growth Index.((CRSP U.S. Large Cap Growth Index))

- Dividend (Income). There are two types of dividend indexes. One features companies with relatively high dividend yields (FTSE High Dividend Yield Index). In contrast, the other tracks companies who consistently raise their dividends and are expected to continue the policy in the future (S&P High Yield Dividends Aristocrats Index).((S&P High Yield Dividend Aristocrats)),((FTSE All-World High Dividend Yield Index))

- Industry sectors. Investors can purchase an index fund composed of companies in a specific industry. Industry examples include the Dow Jones U.S. Financials Index (financial companies), MSCI U.S. Investable Market Consumer Discretionary 25/50 Index (Consumer-oriented), Utilities Select Sector Index (utilities), and ISE Cloud Computing Index (companies focused on cloud computing).((Dow Jones U.S. Financials Index)),((MSCI US Investable Market Consumer Discretionary 25/50 Transition Index (USD))),((Utilities Select Sector)),((ISE CTA Cloud Computing Index (CPQ)))

Bond Index Funds

Those who prefer to purchase debt for long-term income can buy debt-focused index funds for diversification. They include the Barclays Aggregate Bond Index (investment-grade bonds with a minimum of one-year maturities ), or one of the Bloomberg Bond Indexes (long-term, intermediate, and short-term maturities).1,((S&P National AMT-Free Municipal Bond Index))

Investors seeking tax-free income should consider a fund that tracks the S&P National AMT-Free Municipal Bond Index.

Leveraged Index Funds

Some investors, not content with an index fund’s average returns, seek to double (2x) or triple (3x) their profits by leveraging their investment with debt or options. The leverage increases the possibility of high returns when the index rises, as illustrated in Table 1.

Table 1 Index Fund vs Leveraged Index Fund

While leverage is advantageous when you are on the right side of the market, volatility can cost a portion of your original investment. Figure 1 demonstrates what happens to the value of the account if the index returns to its initial level, i.e., 1000.

While the investor in the non-leveraged index fund is unaffected by the volatility, the investor in the 3x leveraged fund has lost 5% of his investment.

Borrowing to buy securities or allowing fund managers to borrow using the fund assets is rarely a successful strategy for long-term investors.

Popular Investment Strategies

The term “investing” is used today to describe anyone and everyone who buys or sells a security.

This interpretation discounts the motive, strategy, or outcomes for the multiple strategies that drive transactions in the stock market.

Economist John Maynard Keynes published his classic book, “The General Theory of Employment, Interest, and Money,” five years after the Wall Street Crash of 1929.((The General Theory of Employment, Interest, and Money))

The Dow Jones Industrial Average fell from 381.17 on September 3, 1929, to 41.22 on July 8, 1932, a drop of almost ninety percent.

The economic devastation forced government leaders, bankers, and economists to implement policies designed to reduce the likelihood of a similar future disaster.

Keynes believed a significant cause of the drop was the imbalance between investors and speculators, the latter dominating the market to make an easy, quick buck and instant riches.

Crowds of citizens borrowed money to buy shares in companies touted by neighbors and enthusiastic stockbrokers. Conmen, stock manipulators, and greedy capitalists operated freely in the laissez-faire market, expecting buyers to protect themselves.

Keynes considered an investor as one who prudently analyzes a company to forecast its future profits.

Speculators preyed on the general public’s naivete and ignorance. Many employed the Greater Fool strategy, “a greater fool will soon appear to buy stock for more than I paid.”

Benjamin Graham – considered by some as the father of security analysis and a tutor of a young Warren Buffett – agreed that unbridled greed and the lack of regulation were significant contributors to the Crash.

He wrote that speculation was “a cause for concern” in his 1949 book The Intelligent Investor, observing that there were many ways in which speculation could be unintelligent.((The Intelligent Investor: The Definitive Book on Value Investing. A Book of Practical Counsel (Revised Edition) ))

In the century since the Roaring 20s that birthed the intersection of Main Street and Wall Street, four investment strategies emerged. Each continues in use today.

Speculation

Milton Friedman, writing in In Defense of Destabilizing Speculation in 1960, noted much of the public equates speculation with gambling, with no value as an investment philosophy.((In Defense of Destabilizing Speculation by Milton Friedman))

However, the economist contended that speculators often have an information advantage over others, enabling them to make profits when others less knowledgeable lose. In other words, speculation is the buying and selling of securities based upon a perceived advantage in information.

Friedman failed to acknowledge that the sources of information advantages have been significantly curtailed, if not eliminated, by securities laws enacted in countries around the world to control “insider trading.”((Insider Trading))

Before the regulations, wealthy investors with connections to corporate personnel could learn confidential, proprietary information unavailable to the public, enabling them to buy or sell stocks with a significant advantage (shooting fish in a barrel).

Inside Information Regulations

Trying to get or using unknown or confidential information to buy and sell a company’s stock can be hazardous to one’s wealth and freedom.

The U.S. Securities and Exchange Commission (SEC) aggressively monitors stock transactions of companies with significant, unanticipated price changes, presuming that those who profit have benefitted from illegal insider information.

The homemaker tv star Martha Stewart spent several months in jail after being judged guilty of insider trading, while sports figures like Phil Mickelson and Mark Cuban have suffered unfavorable publicity with claims of trading on confidential information.((Martha Stewart Settles Civil Insider-Trading Case)),((Gambling legend Billy Walters blames Phil Mickelson for his 5-year prison sentence)),((Not guilty: Cuban acquitted of insider trading))

A speculator requires a big bankroll and a strong constitution since, in most cases, they act contrary to general market trends. When they are right, they personify the wag’s investment advice to “buy low, sell high.”

Paul Mladjenovic, the author of four editions of “Stock Investing for Dummies,” explained the point of speculation best:

You’re putting your money where you think the rest of the market will be putting their money – before it happens.((Stock Investing For Dummies))

While people still speculate on stocks, relying upon rumors and their intuition, the strategy is unlikely to deliver consistent profits over the long term, making it inappropriate for those seeking to save for retirement or other life goals.

For those who cannot resist wagering from time to time, remember that the odds are against you, whether in a casino or the stock market. Don’t spend more than you can afford to lose without affecting your lifestyle or attaining your life goals.

Technical Analysis

Jesse Lauriston Livermore, named the “most fabulous living U.S. stock trader” in a 1940 TIME article, developed his skill buying and selling stocks in bucket shops – unregulated businesses that were the equivalent of today’s off-track betting parlors, where customers placed wagers on the price movement of stocks.((Business: Boy Plunger))

Livermore’s ability to detect and interpret patterns in the movements of stock prices quickly made him persona non grata in the shops, much like card counters are banned from the casinos of Las Vegas and Atlantic City today.

Livermore’s focus on the patterns of a stock’s price changes led to the identification of “pivot points,” what we call levels of support and resistance today.

He purchased shares as they rebounded from a support level and sold them when they approached a resistance level.

Livermore understood that stocks move in trends but recognized that the pattern might suddenly change direction depending upon the mood of stock market participants.

He also warned that no trading strategy could deliver a profit of 100% of the time. If a trend cannot be identified, investors should be out of the market until an opportunity for profit is readily apparent.((Reminiscences of a Stock Operator))

The Livermore strategy evolved into today’s technical analysis.

Technicians led by John Magee and Roberts Edwards – authors of “Technical Analysis of Stock Trends” – claimed that intrinsic values – the theoretical worth of a business based on careful analysis of information – does not affect prices in the short-term, but the aggregate beliefs of the investing public about a company’s future profits, even if incorrect.((Technical Analysis of Stock Trends))

They suggested that investors’ various actions – buying shares, selling shares, or holding their positions – were reflected in patterns of stock prices that reflected investor psychology, patterns that continuously repeated themselves.

A review of previous prices and their associated volumes of shares produced identifiable graphic formations – support and resistance levels, head-and-shoulder patterns, pennants, flags, and double tops or bottoms – that, correctly interpreted, could generally project future prices.

Popularity of Trading

Advances in technology, lower commission rates, and the appearance of online brokerage firms have enabled individuals to employ technical analysis systems of increasing sophistication to follow and interpret the market.

While speculators attempt to forecast future prices by intuition or an information advantage, traders seek to identify existing trends to make a small profit before the trend ends.

Speculators go to the train depot and board trains before they embark; traders rush down the concourse looking for a train that is moving – the faster, the better – and hop on, hoping for a good ride.

The bulk of trading occurs through financial institutions’ programmed systems to analyze price trends and place orders when specific criteria are reached. Sometimes referred to as “algorithmic or high-frequency trading (HFT),” computers identify market patterns and buy or sell securities in a matter of milliseconds.

High-frequency traders can make profits of a penny or less per share, substantially magnified by transactions that involve millions of shares.

The impact of high-frequency trading and the firms engaged in the activity remains controversial.

There are also concerns that automated trading reduces market liquidity and exacerbates major market disruptions, such as the May 6, 2010, market crash, and recovery – the Dow Jones Industrial Average dropped 998.5 points (9%) in 36 minutes.

A similar crash happened on August 24, 2015, when the Dow fell more than 1000 points at the market open. Trading was halted more than 1,200 times during the day to calm the markets.

Day Trading

As technology and communications have fallen, many individuals have attempted to emulate the big banks and financial firms.

They buy and sell securities within a short time, often holding a position less than a single trading day. While few individuals have the financial ability to emulate the trading habits of the big institutions, day trading is a popular strategy in the stock market.

Many become day traders due to day trading training firms’ enticement, an unregulated industry that profits from the sale of instruction and automated trading software to their customers.

The sales materials falsely imply that the software is like the sophisticated, expensive software programs used by the big traders, such as Goldman Sachs or JP Morgan Chase.((How a Goldman Sachs trader can make $100 million in the Volcker Rule era)),((Trading 2020: Then, Now & Beyond))

Day trading typically involves tens of trades each day, hoping for small profits per trade, and the use of margin – borrowed money – from the brokerage firm.

The SEC has issued special warnings to deter individual day traders. Also, day traders are subject to additional margin requirements if they exceed four or more day trades in five days.((Day Trading: Your Dollars at Risk)),((Day-Trading Margin Requirements: Know the Rules))

Despite the number of new day traders entering the market each year, many securities firms and advisors openly discourage the strategy.

The Motley Fool claims that

day trading isn’t just like gambling; it’s like gambling with the deck stacked against you and the house skimming a good chunk of any profits right off the top.((Why Day Trading Stocks Is Not the Way to Invest))

Technical analysis is not a practical investment strategy for most people since its objectives are short-term profits, utilizes expensive computing and communication technology, increases investment risk through leverage, and requires the full-time attention of the investor. Individual traders must compete with professional traders with technological advantages and extensive capital resources. Those who are confident that their trading skills are exceptional should remember that an estimated 99% of traders lose their investment, traders who also believed they could beat the system.((Day Trading: Smart Or Stupid?))

Fundamental Analysis (Buy and Hold)

Graham defined an investor as a stock buyer who intends to be a long-term owner of the companies in which they purchase shares.

Investment advisers and stock analysts spend hour after hour analyzing company after company to identify those with the most popular products or services, efficient production and delivery systems, and an astute management team.

Their investment goal is to find diamonds in the rough, the companies with the highest future earnings stream that can be purchased at the highest discount from real value.

Benjamin Graham is credited with the development of fundamental analysis, the analytical techniques, and standards used to identify stocks to buy and hold.

Graham was primarily concerned with the metrics of companies, including price-earnings ratios, dividend rate, debt, and earnings growth per share.

Warren Buffett explained his motive in buying a security:

You look to the asset itself to determine your decision to lay out some money now to get some more money back later on… and you don’t really care whether there’s a quote under it [at] all.

When Buffett invests, he doesn’t care whether they close the market for a couple of years since an investor looks to a company for what it will produce, not what someone else may be willing to pay for the stock.

Warren Buffett refined Graham’s methods, noting that understanding “accounting numbers are the beginning, not the end, of business valuation.”

He looks for companies that dominate their industry so they will make profits year after year in good or bad political or economic environment. He always intends to hold an investment long-term.

Some market participants might consider an investing philosophy based on conservative stocks with long holding periods to be out-of-date and boring.

They would do well to remember the words of Paul Samuelson, Nobel winner in Economic Sciences, who advised,

Investing should be more like watching paint dry or grass grow. If you want excitement, take $800 and go to Las Vegas.

Managed Securities Portfolios

Frustrated by inconsistent returns and the time requirements to effectively implement either a fundamentalist or technical strategy, investors increasingly turned to professional portfolio management through mutual funds.

The advantages of the mutual funds over the analysis, selection, and maintenance of individual stocks were clear: professional management, long holding periods, and diversification.

From 1980 to 2000, the number of households that owned a mutual fund directly or in an employer-sponsored retirement plan grew from 4.6 million to 48.6 million.

According to the Investment Company Institute, almost 102 million individuals owned one or more mutual funds by in 2019, about the same as the year 2000.

Many market observers attribute the stagnant growth of mutual fund ownership in the last two decades to the academic studies that began to appear in the early 1970s.

In 1970, University of Chicago finance professor Eugene Fama, a Nobel Prize winner, challenged the validity of technical and fundamental analyses.

He claimed that modern securities markets are incredibly efficient and that all information is reflected in a security’s price, neither fundamental nor technical analysis can help an investor achieve higher returns than a randomly selected portfolio of individual stocks.((Efficient Capital Markets: A Review of Theory and Empirical Work))

Despite the shortcomings of a fundamental strategy – the need for expertise in collecting and analyzing reams of financial records and government reports – most investing experts agree that the approach is better suited to the average investor than either speculation or technical analysis. While investing in a mutual fund transferred management responsibilities to others, most fund managers practiced Graham’s and Buffett’s fundamental analysis to select the stocks in their portfolios. Unfortunately, many managers, prodded by aggressive salespeople, over-sell their capabilities, suggesting that they can beat market averages.

Index Fund Investing – A New Strategy

Fama’s ideas became popularly encapsulated as the Efficient Market Hypothesis (EFH). Influenced by the studies of Fama and Samuelson, Bogle founded the Vanguard Group and created the first passively managed index fund in 1975.((The Efficient Market Hypothesis – Definition, Theory & What It Means For Your Investing))

Despite the industry skeptics about index investing, Bogle’s faith in index investing was unshaken.

He explained his logic in “The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns.”((The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns))

- Investors, as a group, cannot outperform the market because they are the market.

- Investors as a group must under-perform the market because the costs of participation – mainly operating expenses, advisory fees, and portfolio transaction costs – constitute a direct deduction from the market’s return.

- Most professional managers fail to outpace appropriate market indexes and those who do so rarely repeat in the future their success in the past.

Since the early studies, others have confirmed Bogle’s assertion that beating the market is virtually impossible.

Dr. Russell Wermers, a finance professor at the University of Maryland and a co-author of “False Discoveries in Mutual Fund Performance: Measuring Luck in Estimating Alphas,” claimed in an article in The New York Times that the number of funds that have beaten the market over their entire histories is so small that the few who did were “just lucky.” He believes that trying to pick a fund that would outperform the market is “almost hopeless.”((The Prescient Are Few))

Professionals’ View of Index Funds

Many of America’s best-known investors agree that index funds are best alternatives for most investor:

- Dr. Charles Ellis. Writing in the Financial Analysts’ Journal in 2014, Ellis said, “The long-term data repeatedly document that investors would benefit by switching from active performance investing to low-cost indexing.”((The Rise and Fall of Performance Investing))

- Peter Lynch. Described as a “legend” by financial media for his performance while running the Magellan Fund at Fidelity Investments between 1977 and 1980, Lynch advised in a Barron’s April 2, 1990 article that “most investors would be better off in an index fund.”((Quotes by Peter Lynch))

- Charles Schwab. The founder of one of the world’s largest discount brokers, Schwab recommends that investors should “buy index funds. It might not seem like much action, but it’s the smartest thing to do.”((We talked to Chuck))

Adherents to index investing are sometimes referred to as “Bogle-heads.” One advantage of buying index funds rather than individual securities is predetermined asset allocation – using diversification to reduce risk in a portfolio.2

Owning a variety of asset classes and periodically re-balancing the portfolio to restore the initial distribution between classes reduces overall volatility and ensures a regular harvesting of portfolio gains.

Stock market profits can be elusive, especially in the short term. Those who seek to maximize their investment returns without incurring undue risk would benefit from an index fund investment strategy.

Cautions about Index Fund Investment

While index funds are ideal for most investors, they have characteristics that might limit their appeal to individual investors. Their limitations include:

Focus on the Long-Term

In the short term, every investment can be overwhelmed by popular sentiment.

Instances, where emotions produce booms and bust, are present throughout history:

- Tulipmania. During the Dutch Tulip Bubble, tulip prices soared twentyfold between November 1636 and February 1637 before plunging 99% by May 1637.((Earl Thompson. “The Tulipmania: Fact or Artifact?” Pages 99–114, Public Choice 130. 2007.)),((Dutch Tulip Bulb Market Bubble Definition))

- Florida real estate. The combination of the Roaring Twenties economic boom and Florida’s beautiful weather and beaches drove up prices for undeveloped swampland to ridiculous heights until crashing n 1925 and devastating the state’s economy.

- Black Monday. The most enormous one day crash of the stock market (22.6% drop in value) happened on October 19, 1987, when a horde of panicked sellers triggered automatic sell orders intended to halt financial institutions’ losses on their stock investments.

Fortunately, reason eventually returns to markets and assets recover. In instances of widespread financial panic, few investments – including index funds – are unaffected, at least temporarily.

Diluted returns

A portfolio of stocks, whether managed or passive, necessarily reflects the average performance of the individual securities in the collection. The trade-off for accepting a diluted return is the reduction in risk through diversification. Only those foolish or confident enough to believe that they can consistently pick the individual stocks that will appreciate the most will consider diversification a disadvantage.

Lack of flexibility

Investors who purchase the securities of individual companies have maximum flexibility in investment actions. They can buy or sell a stock for any reason without any regard to their holding period.

Those who buy managed portfolios expect the managers to continually adjust the composition of the portfolio based on changing market conditions.

In contrast, an index fund holder cannot affect the portfolio in any manner; their only power is to buy or sell their holdings.

All investors should understand that no one has discovered or developed an investment philosophy or strategy that is valid 100% of the time. Investment gurus come and go, praised for their acumen until the inevitable happens, and they join the roster of previously humbled experts. For most people, index fund investing is as close to a perfect strategy as possible. The advantages of index funds – diversification, low cost, and high return – vastly outweigh their disadvantages. An index fund provides as close to a worry-free investment as possible in a constantly changing technological, economic, and political environment.